Two Proven Methods. One Personal Journey. Here’s What Actually Helped Me Get Debt-Free.

Drowning in Debt & Googling Late at Night

I remember the night clearly — sitting on my bed, laptop glowing, heart pounding. My credit card balance had just crossed $11,000. Between student loans, car payments, and random purchases I’d justified over the years, I was juggling five different debts. The stress was real.

In my desperate search for a plan, I found two terms:

Debt Snowball and Debt Avalanche.

Both seemed smart. Both promised freedom. But I could only pick one to start.

This is the story of which I chose, why, and what actually worked in real life — not just on paper.

The Two Titans: Debt Snowball vs. Debt Avalanche

Before I get personal, let’s break these down clearly.

🧊 Debt Snowball Method:

Pay off your smallest debts first, regardless of interest rate.

Psychology-driven. Wins come fast, and momentum builds.

Example:

If you owe $200, $1,000, and $5,000 — you attack the $200 first.

🔥 Debt Avalanche Method:

Focus on the highest-interest debt first, regardless of balance.

Mathematically optimal. You save the most money in interest.

Example:

If you owe 18% interest on one card and 6% on another, the 18% gets crushed first — even if it’s a bigger amount.

My Situation: Emotion vs. Math

On paper, the avalanche method made perfect sense. My highest interest card was nearly 25%. It was bleeding me dry. But here’s the problem:

The balance was huge — over $7,000.

I started paying it… and after 2 months, the needle barely moved. I was still surrounded by other debts. My motivation dipped. I started missing payments again.

The Pivot: Enter the Snowball

Out of frustration, I switched to the Debt Snowball method.

Here’s what I did:

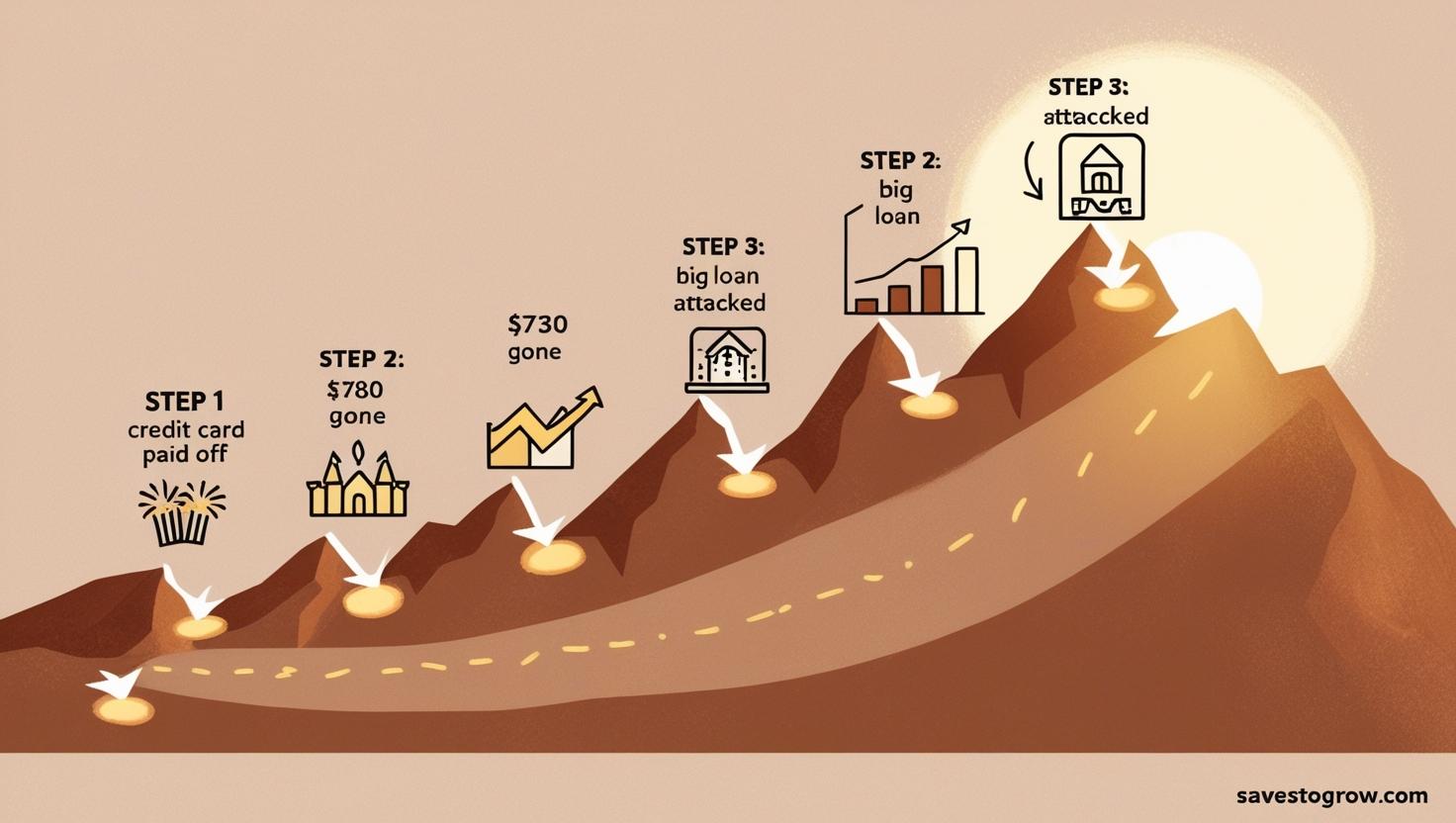

- Listed all my debts from smallest to largest.

- Paid the minimum on everything.

- Dumped every extra dollar into the smallest one — a $280 credit card.

I paid that off in 2 weeks.

It felt like a win.

Something shifted inside me.

Then I tackled the next one: $730.

Gone in a month.

I started getting addicted to the feeling of closing accounts. For the first time, I felt in control.

Momentum Is a Powerful Drug

Within 6 months:

- 3 of my 5 debts were completely paid off.

- My credit score jumped by 70 points.

- I started budgeting religiously (never thought I’d say that).

The confidence I gained made it easier to face the bigger, uglier debts. By the time I got to the high-interest loan, I had room to breathe, and more monthly cash to throw at it.

“It wasn’t the most logical path. But it was the one I could stick to.”

Final Numbers: Snowball Results vs. Avalanche Theory

| Method | Total Time | Interest Paid | Emotional Resilience |

|---|---|---|---|

| Avalanche (estimated) | ~18 months | ~$2,100 | ❌ Burned out fast |

| Snowball (actual) | ~21 months | ~$2,800 | ✅ Motivated start to finish |

Yes, I paid a bit more in interest.

But I finished.

That matters more.

Lessons Learned (The Hard Way)

- Math doesn’t matter if you quit halfway.

- Your brain needs small wins. Snowball gave me that.

- Behavior > spreadsheets.

- Debt is not just numbers — it’s emotional warfare.

FAQ: Common Questions People Ask Me

Q: Did you ever switch back to Avalanche?

Not really. But once I got down to one big loan, I used Avalanche logic to kill it faster.

Q: Did you use any apps?

Yes! I used the web app CalculatesNow ( It calculates in INR, but I managed that )— it let me track both methods and compare them in real-time. Super helpful.

Q: What if I’m disciplined? Should I still use Snowball?

If you’re 100% committed and emotionally detached from money, Avalanche is more efficient. But most of us aren’t robots.

Q: How did you find extra money to pay off debt?

I sold stuff on Facebook Marketplace, canceled 3 subscriptions, and started freelancing on weekends. Small moves added up.

Final Word: Pick the Plan You’ll Finish

If you’re stuck deciding between Snowball and Avalanche, ask yourself this:

“Do I want to be right? Or do I want to be free?”

The avalanche may win on spreadsheets. But for me, the snowball helped me win in real life.

I’m now completely debt-free. And honestly?

That $280 credit card was the best debt I ever crushed.

Sources

- Dave Ramsey: The Debt Snowball Explained

- NerdWallet: Debt Avalanche vs. Snowball