Most tax loopholes don’t belong to the ultra-rich.

Some are hiding right under your nose—quiet, legal, and built exactly for people like you.

This article is your playbook if you’re middle class and feeling squeezed by taxes. We’re cutting through the clutter and showing you 5 overlooked deductions that could put up to $5,000 back in your pocket—no shady tactics, no CPA required.

Let’s break it down.

1. State Sales Tax Deduction (Yes, Even for Regular Folks)

What it is:

You can deduct either your state income tax or your state sales tax—whichever is higher.

Why it matters:

If you live in a state with low (or zero) income tax, like Florida, Texas, or Washington, this deduction can be a goldmine. Big purchases like appliances, furniture, or home renovations push your total sales tax high enough to make it worth deducting.

Example:

You bought a used car for $18,000. At 8% tax, that’s $1,440 in sales tax—just from one purchase.

How to claim it:

Use the Schedule A form and the IRS’s optional Sales Tax Deduction Calculator online. No receipts required (but keep the big ones just in case).

Savings potential:

$1,000+ if you itemize and live in the right state.

2. Home Office Deduction (Even If You’re an Employee Side-Hustler)

What it is:

A deduction for the portion of your home used exclusively for work—even a side gig or freelance project qualifies.

Why it matters:

The IRS lets you deduct a percentage of your rent, utilities, internet, repairs, and even depreciation.

Here’s the catch:

If you’re a W-2 employee, you can’t claim it. But if you’ve got any 1099 side income (freelance, tutoring, consulting, Etsy, YouTube), you’re in the clear.

Example:

A 100 sq ft office in a 1,000 sq ft apartment = 10% of eligible expenses.

How to claim it:

Use Form 8829 or go with the simplified method: $5/sq ft up to 300 sq ft.

Savings potential:

Up to $1,500 if you’re strategic.

3. Lifetime Learning Credit (Education Isn’t Just for Kids)

What it is:

A credit (not deduction!) of up to $2,000 for qualified education expenses.

Why it matters:

It’s for anyone taking college-level courses to upgrade skills—yes, even adult learners and part-timers.

You qualify if:

- You’re enrolled in eligible institutions

- You paid out-of-pocket (or via loans)

- Your income is under $90K (single) or $180K (married filing jointly)

Example:

Taking a $3,000 online course at a local college? Boom—$2,000 credit, directly reducing what you owe.

How to claim it:

File Form 8863 with your 1040. Keep proof of tuition payments.

Savings potential:

Flat $2,000 tax credit—off the top of your bill.

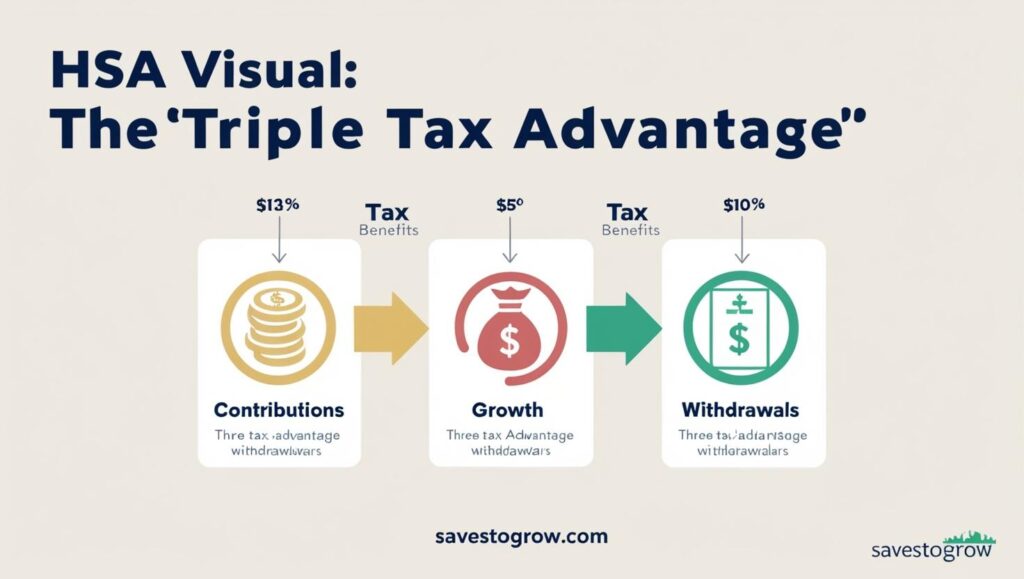

4. Health Savings Account (HSA): Triple Tax Win

What it is:

An account you contribute to pre-tax, grow tax-free, and use tax-free for medical expenses.

Why it matters:

If you have a high-deductible health plan (HDHP), you’re eligible. Contributions reduce taxable income. Earnings grow tax-free. Withdrawals (for health stuff) are tax-free. It’s the IRS unicorn.

Example:

You contribute the 2024 limit: $4,150 (single). You save $900+ in taxes upfront—and more in growth over time.

How to claim it:

Open an HSA through your bank or employer. Contributions show up on Form 8889.

Savings potential:

$900–$1,500 annually, depending on your tax bracket.

5. Saver’s Credit: Free Money for Retirement Contributions

What it is:

A little-known credit for low-to-middle-income folks who contribute to a 401(k) or IRA.

Why it matters:

You get up to $1,000 back (or $2,000 for married couples)—just for investing in your future.

You qualify if:

- You’re 18+

- Not a full-time student

- Income under $36,500 (single) or $73,000 (married)

Example:

You contribute $2,000 to your IRA. If your income is low enough, you get a 50% credit = $1,000 back.

How to claim it:

File Form 8880. Use tax software—it catches this if you’re eligible.

Savings potential:

Up to $2,000 per household.

Final Word: These Loopholes Aren’t Dirty—They’re Designed for You

Let’s call them what they really are: middle-class tax tools. The IRS built these to support working people—those hustling on the side, saving for retirement, learning new skills, or just trying to stay ahead.

Used right, these 5 loopholes can add up to $5,000+ in real savings. All legal. All IRS-approved. All within reach.

Don’t leave that kind of money on the table.

FAQ: Tax Deductions for Middle Class

Q: Do I need a CPA to claim these deductions?

No. Most tax software like TurboTax or FreeTaxUSA walks you through it.

Q: What if I don’t itemize?

Some of these (like the Saver’s Credit or Lifetime Learning Credit) apply even if you take the standard deduction.

Q: Are these loopholes audited more?

Not if you’re honest and have records. They’re common, legal deductions.

Q: Can I claim these retroactively?

Yes—if you’re amending past returns (up to 3 years back). Use Form 1040-X.