I didn’t grow up budgeting. I learned the hard way—through overdraft fees.

After hitting financial rock bottom in my mid-20s, I promised No more blind spending. That led me to budgeting apps. I tried five of the most recommended ones. Some helped. Others made me rage quit.

Here’s what worked, what didn’t, and what I’d recommend to someone serious about controlling their money.

Why Use a Budgeting App?

Because spreadsheets don’t remind you, and your memory lies.

Budgeting apps give you:

- Real-time awareness of where your money’s going

- Automatic tracking from your bank and cards

- Spending alerts to avoid mindless swipes

- Structure to hit financial goals faster

I tested each app for 2–4 weeks, linked real accounts, and tracked spending categories like groceries, rent, eating out, and subscriptions.

1. You Need a Budget (YNAB)

Rating: ★★★★★ (5/5)

Cost: $14.99/month or $99/year

The Good:

- Forces you to assign every dollar a job (zero-based budgeting)

- Crystal-clear categories

- Long-term goal planning (car, vacation, emergency fund)

- Serious behavior change—this is budgeting with discipline

The Bad:

- Steep learning curve

- No free version beyond a 34-day trial

Final Take:

Best for control freaks (in a good way). If you’re truly ready to stop living paycheck to paycheck, YNAB is the upgrade.

2. Mint (Discontinued, but here’s what it was)

Rating: ★★☆☆☆ (2/5)

Cost: Free

The Good:

- Beautiful dashboard

- Auto-categorizes expenses

- Useful credit score tracker

The Bad:

- Constant ads and product pushes

- Sluggish syncing

- Random miscategorizing

Final Take:

It had potential, but bloat and bugs made it unusable. It’s now shut down and replaced by Credit Karma Money, which isn’t a real budgeting tool.

3. EveryDollar (Dave Ramsey)

Rating: ★★★☆☆ (3/5)

Cost: Free (manual); $79.99/year for automation

The Good:

- Simple, clean layout

- Great for envelope-style, zero-based budgeting

- Encourages monthly planning and review

The Bad:

- The free version requires manual entry of every transaction

- Limited customization unless you pay

- Feels rigid if you’re not following Ramsey’s system

Final Take:

Perfect for someone who wants to budget like it’s 1995—but on an app.

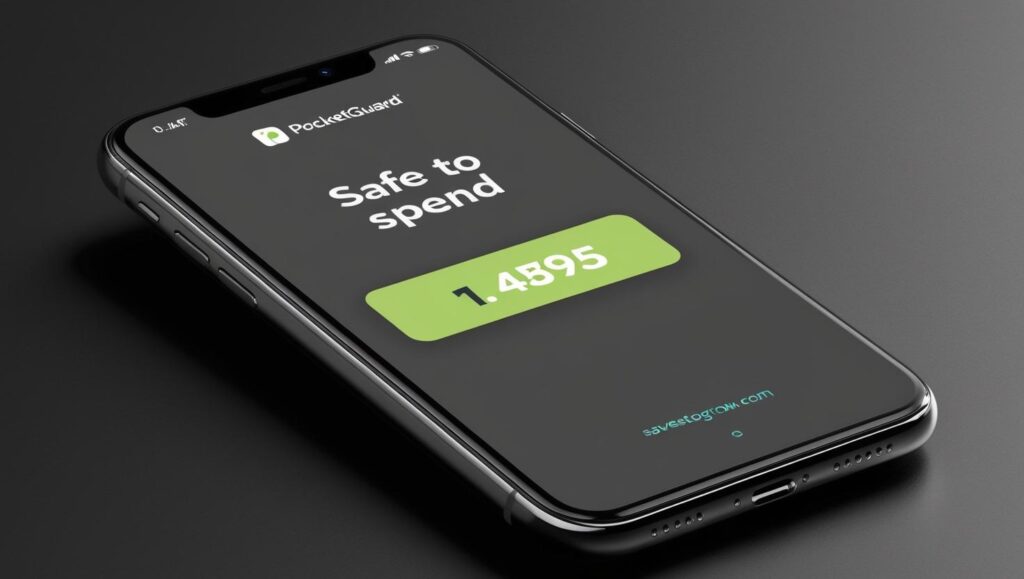

4. PocketGuard

Rating: ★★★★☆ (4/5)

Cost: Free with optional $7.99/month upgrade

The Good:

- Tells you what’s safe to spend after bills & goals

- Automatic syncing and categorization

- Useful for casual users

The Bad:

- Limited long-term planning tools

- Ads and upsells can feel intrusive

Final Take:

Excellent for beginners or anyone who wants budgeting without the math headache.

5. Goodbudget

Rating: ★★★☆☆ (3/5)

Cost: Free (basic); $8/month or $70/year for full version

The Good:

- Classic envelope method done digitally

- Great for couples/shared budgets

- No bank linking—manual for privacy

The Bad:

- Manual entry gets old fast

- No real-time account syncing

- Feels outdated in design

Final Take:

Nice for privacy-focused or old-school users, but not for busy people who want automation.

My Top Picks by Use Case

| Goal | Best App |

|---|---|

| Serious budgeting | YNAB |

| Beginner-friendly | PocketGuard |

| Manual entry / envelope style | Goodbudget |

| Simple + faith-based budgeting | EveryDollar |

What I Use Now

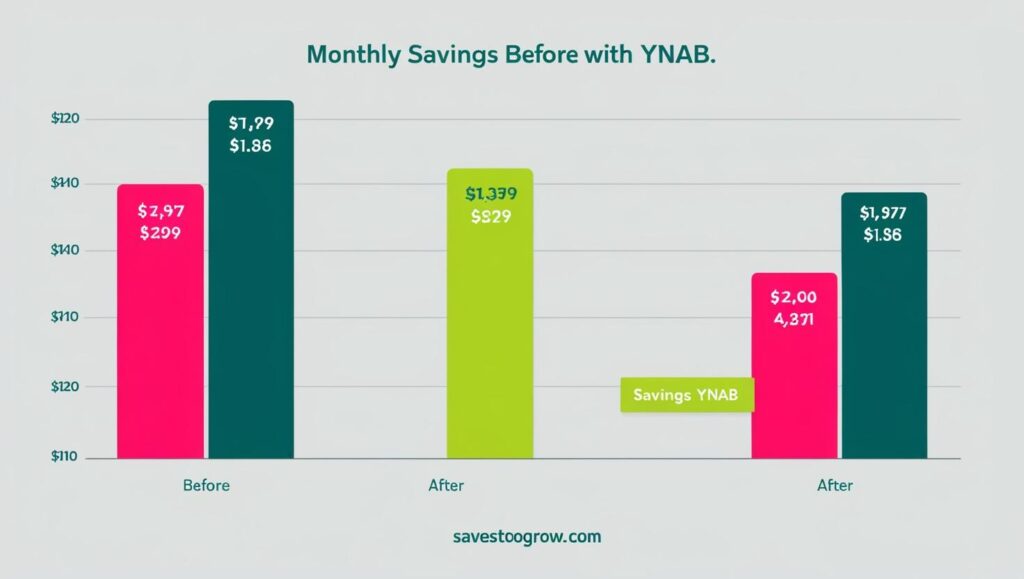

After testing them all, I landed on YNAB. Yes, it costs money. But I’ve saved over $3,200 since switching—and finally built a 3-month emergency fund.

It’s not about the app. It’s about having a system that works with your brain. For me, that system had to be visual, disciplined, and future-focused.

FAQs

Q: Should I pay for a budgeting app?

Yes, if it saves you more than it costs (YNAB did that for me within 3 weeks).

Q: Can’t I just use Excel or Google Sheets?

You can. But most people don’t stick with it unless they’re already spreadsheet lovers.

Q: What’s the best app for couples?

Goodbudget or YNAB. Both allow shared budgeting and goal tracking.